Trump Account overview

The Trump Account is a new type of traditional IRA, or tax-deferred investment account, with special rules for eligible U.S. children under the age of 18. U.S. citizen children born on or after January 1, 2025, and on or before December 31, 2028, are eligible to receive a one-time $1,000 contribution from the U.S. Department of the Treasury, deposited directly into their Trump Account.

Activate an account

You must complete IRS Form 4547 in the app or through the official IRS website to elect to open a Trump Account for your eligible children.

To complete IRS Form 4547 through the IRS website, you will first need to verify your identity with ID.me. This helps protect your information and provide secure access to IRS online account services. You’ll need to provide dates of birth, contact information, and Social Security numbers for you and your child. After you’ve completed the IRS form, check out Activate an account for more details on eligibility and next steps.

Investment options

Trump Account contributions will be invested automatically in a default exchange-traded fund (ETF) that provides broad exposure to U.S. companies, allowing the investment to grow over time as those companies grow. All contributions will be automatically invested in SPYM, an index fund that tracks the S&P 500 by holding hundreds of the largest U.S. companies.

Please note that investments in the program are not guaranteed by the U.S. government and are subject to market risk.

Track contributions

After your child’s Trump Account is activated and can accept contributions, you can track all account transactions, such as contributions in the account’s history in the app.

Future return calculator

To help you visualize the effects of compounding interest on your potential account returns over time, you can use the Future return calculator to view future growth potential.

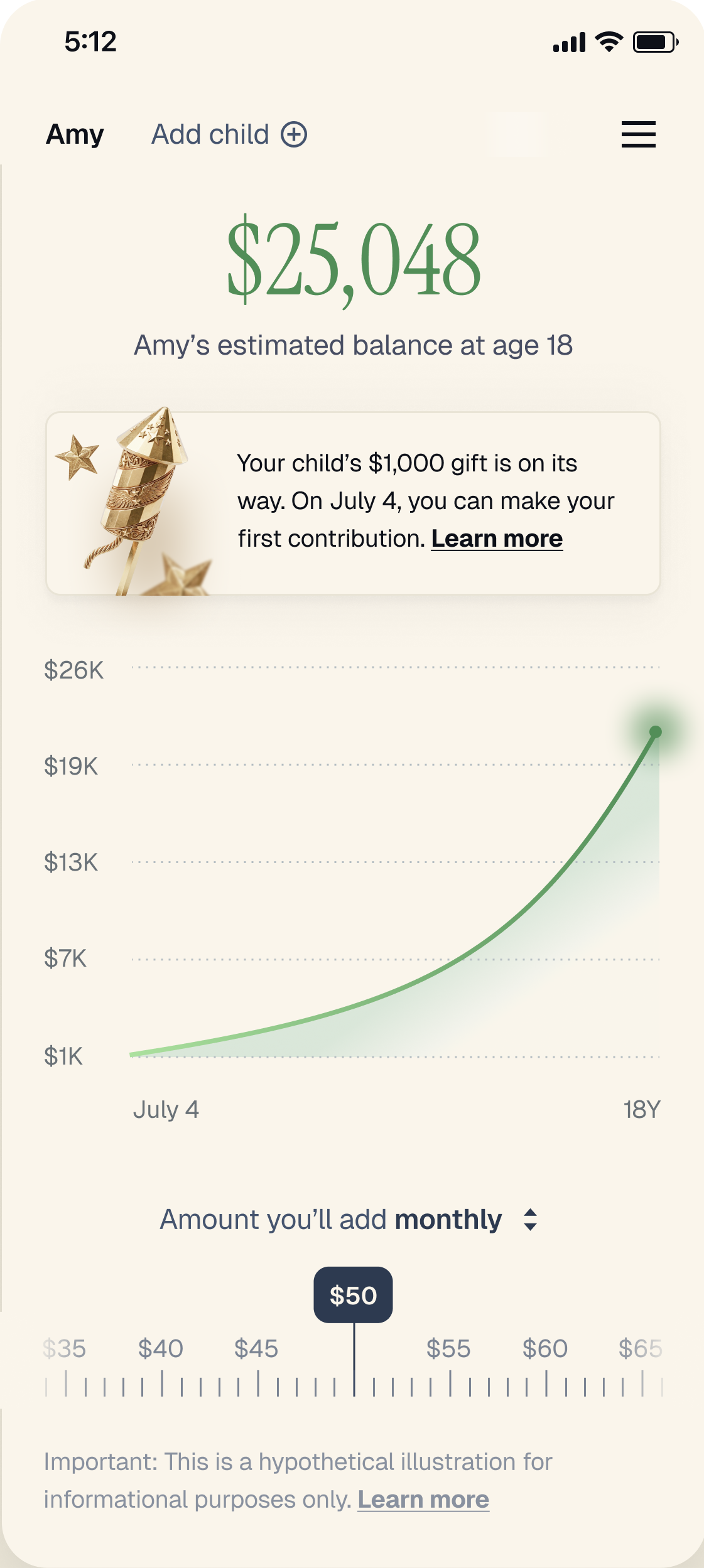

The following shows an example of how your child’s account can grow over time.

Hypothetical examples and other assumptions

- Assumes the account starts with the $1,000 pilot program contribution from the U.S. Department of the Treasury

- You make a $50 monthly contribution

- The child is a newborn when the contributions are made, allowing 18 years for compound growth

- The account earns an average rate of return of 7%

- You could have as much as $25,048

- The illustration doesn’t account for potential changes to contribution limits in the future

Account returns are not guaranteed and this illustration is hypothetical and not intended to represent an exact account value at any given time. Note that this example does not account for the impact of inflation, contribution changes, withdrawals, or any potential dividends.

FAQ for everyone

Authorized individuals (such as parents, guardians, adult siblings, or grandparents) can elect to open an account for eligible children. If you are electing to open the account and applying for the $1,000 pilot program contribution, you must be an individual who anticipates that the eligible child will be your "qualifying child" for tax purposes for the year that you are making the election.

Only one Trump Account may be opened per child. If the IRS processes more than one election, the first authorized individual to complete account activation becomes the responsible party, and additional activation attempts for that child will no longer be eligible.

For jointly filed tax returns, the primary taxpayer may be required to complete activation and serve as the responsible party. If the other spouse would like to serve as the responsible party instead, they can submit a new IRS Form 4547 in their own name or be added as a trusted contact on the account. A responsible party change process is also available by contacting customer support.

The account is legally owned by the child (minor under the age of 18) but is managed by a responsible party (such as a parent or legal guardian). Minors are not allowed by law to manage the account until they reach age 18.

Beginning July 4, 2026, anyone can contribute to a child’s Trump Account. Parents, family, and friends can add up to a combined total of $5,000 per year to an eligible child’s account. Employers can contribute up to $2,500 per year, per employee, which counts toward the $5,000 annual limit. Other donors, including non-profit organizations as well as state and local governments, can also contribute to these accounts. Qualified class contributions from non-profit donors or government add extra support and don’t count towards the annual contribution limit.

Parents, family, and friends can make cash contributions to a Trump Account beginning July 4, 2026 through the contribution options available in the app.

Employers may also make contributions through an employer contribution process, when available. Qualified class contributions from approved donors, including eligible non-profit organizations and state or local governments, may also be deposited into eligible accounts.

Eligible children will also automatically receive the one-time $1,000 pilot contribution from the U.S. Department of the Treasury. This contribution does not count toward the account’s annual $5,000 contribution limit.

Asset transfers through the Automated Customer Account Transfer Service (ACATS) or rollover funds or assets from a different type of savings account like a 529 or custodial IRA are not supported. Check out Link accounts for details about linking a bank or debit card for account funding.

The money is automatically invested and held in a dedicated trust account with a registered trustee, with all securities transactions cleared through the Depository Trust and Clearing Corporation (DTCC). This program operates in partnership with a federal record keeper and banking partner. Additionally, your child's investments are protected by SIPC coverage up to $500,000 based on your child’s information. Keep in mind though that SIPC does not protect against losses due to market fluctuations. Explanatory brochure available upon request or at www.sipc.org.

Funds in Trump Accounts will generally remain invested and are not available for withdrawal before the child reaches age 18. Until December 31 of the calendar year in which the child (account beneficiary) reaches age 17, the account has a $5,000 annual contribution limit that is separate from other IRAs that the child may have.

Until the child (account beneficiary) reaches age 18, the following rules apply:

- Can only be invested in eligible investments, and

- Distributions are generally restricted from the account.

Note that after December 31 of the year the child turns 17, no new contributions can be made until the child reaches the age of 18 and the account transitions to a traditional IRA.

After the child (account beneficiary) reaches age 18, the strict block on account withdrawals ends, and the account transitions to, and must follow the standard rules of a traditional IRA. For example, after this time, funds withdrawn from the account can be used without a 10% early distribution tax for certain eligible expenses, such as higher education expenses or a down payment on a first-time home purchase (up to $10,000 lifetime), subject to ordinary income tax but without an additional distribution tax.

A child can also keep the money invested in the account and continue to let it grow, providing potential long-term financial security later.

Trump Accounts, 529 plans, and other child savings accounts each serve different purposes and may complement one another. A 529 plan provides significant tax advantages for families saving primarily for qualified education expenses. A Trump Account is designed to encourage long-term investing for children and offers different contribution opportunities and withdrawal rules. Depending on your family's financial goals, one or several account types may be appropriate.

A unique benefit to Trump Accounts is the one-time $1,000 pilot program contribution from the U.S. Department of the Treasury. Children born during 2025 through 2028 may be eligible to receive this contribution if an election is made by filing IRS Form 4547 and the child meets the eligibility requirements. Employers, qualified charitable organizations, and state and local governments may also make eligible contributions to Trump Accounts. These contribution opportunities are not available for most other child savings accounts.

These contributions receive tax treatment that differs from contributions to 529 plans.

529 plans are designed to encourage saving for qualified educational expenses and provide valuable tax benefits when used for those purposes. By comparison, after a Trump Account transitions to a traditional IRA at age 18, distributions generally follow the rules applicable to traditional IRAs and may be used for a broader range of purposes, subject to applicable tax rules and penalties.

Unlike a custodial IRA, a Trump Account does not require the child to have earned income before age 18 to receive contributions. After the account transitions to a traditional IRA at age 18, future contributions are subject to the eligibility requirements and contribution limits that apply to traditional IRAs.

529 plans and custodial IRAs cannot be rolled over into a Trump Account.

Same as other traditional Individual Retirement Accounts (IRAs), Trump Account earnings are tax deferred and will remain tax deferred until the money is eventually withdrawn. This means the child won’t pay taxes on investment gains on an annual basis as long as the funds remain invested in the account. After the account transitions from a Trump Account to a traditional IRA without the special rules, when the child reaches age 18, the distributions (withdrawals) of any account earnings, pilot contributions, or qualified general contributions are subject to ordinary income tax. A 10% early distribution tax may apply if the beneficiary is under age 59½ when the withdrawal occurs (unless an exception applies).

Note that individual contributions are after-tax (no upfront deduction), while employer and government contributions are generally pre-tax. The contributions made by individuals (parents or family) are considered "basis" and are tax-free when withdrawn. However, distributions (withdrawals) cannot typically be made until the beneficiary (the child) reaches age 18. Account earnings are tax-deferred, not tax-free. Distributions (withdrawals) of account earnings and employer or government contributions are subject to ordinary income tax upon withdrawal. A 10% early distribution tax may apply if the beneficiary is under age 59½ when the withdrawal occurs.

You’ll get an IRS Form 5498-TA for contributions made to the account for the applicable tax year. For permitted distributions, you’ll receive an IRS Form 1099-R.

Trump Accounts are currently only available in US English. For assistance with translations, we recommend using a trusted translation service.

FAQ for parents

You can elect to open an account in one of the following ways:

- You or your tax preparer can file IRS Form 4547 with your federal tax return

- You can go to the Trump Accounts app or the trumpaccount.com website

- File the IRS Form 4547 through the official IRS website by creating an IRS online account

If you completed IRS Form 4547 when you filed your 2025 taxes this year, then you’re all set. If not, you can file in the app or through the IRS website. Note that you must use the same email address and password you entered when you filed the IRS form when activating an account.

No problem. You can file IRS Form 4547 and elect to open a Trump Account for your eligible child or children at any time in the Trump Accounts app, at trumpaccount.com, or through the official IRS website.

Yes! This account belongs to a child and is intended to provide a starting point for their savings.

Your child’s Trump Account contributions will be invested automatically in a default exchange-traded fund (ETF) that provides broad exposure to U.S. companies, allowing the investment to grow over time as those companies grow. All contributions will be automatically invested in SPYM, an index fund that tracks the S&P 500 by holding hundreds of the largest U.S. companies.

Please note that investments in the program are not guaranteed by the U.S. government and are subject to market risk.

Authorized individuals must first elect to open a Trump Account using IRS Form 4547. Once an election is processed, there are no fees to activate or maintain the account, including when contributions are made or invested. All contributions go into the account at no cost to the responsible party or the account beneficiary. However, the investments in the account may be subject to management fees (also called expense ratios). These fees, which cannot exceed more than 0.1 percent of the balance of the investment, are charged by the funds.

Funds remain invested in the account and any returns will be reinvested to take advantage of compounding. This long‑term investment approach is designed to help accounts grow steadily until a child reaches age 18.

No. Earnings in Trump Accounts are tax-deferred, meaning the child does not pay taxes on investment gains each year as long as those earnings remain in the account. This allows more money to stay invested and continue growing over time.

Note that individual contributions are after-tax (no upfront deduction), while employer and government contributions are generally pre-tax. The contributions made by individuals (parents or family) are considered "basis" and are tax-free when withdrawn. However, distributions (withdrawals) cannot typically be made until the beneficiary (the child) reaches age 18. Account earnings are tax-deferred, not tax-free. Distributions (withdrawals) of account earnings and employer or government contributions are subject to ordinary income tax upon withdrawal. A 10% early distribution tax may apply if the beneficiary is under age 59½ when the withdrawal occurs.

Only one Trump Account may be opened for each eligible child.

If more than one authorized individual completed IRS Form 4547 for the same child and the IRS processes more than one election, the first authorized individual to complete account activation will become the responsible party for the account. Once the account is activated, additional activation attempts for that child will no longer be eligible.

For elections made through a jointly filed tax return, the primary taxpayer associated with the IRS filing may be required to complete the account activation process and serve as the responsible party. If the other spouse would like to serve the responsible party instead, they may have to submit a new IRS Form 4547 in their own name, or they may be added as a trusted contact on the account. A responsible party change process is also available by contacting customer support.

No, currently only the responsible party who is managing the account for the child can log in with their credentials. We’re working on allowing read-only access to a designated trusted contact to view your child’s account in the future.

If the responsible party passes away, you’ll need to contact us for assistance. We’ll ask you for an official copy of the death certificate, and we’ll provide you with instructions on how to securely upload it through our portal. We’ll also need details about the person who will manage the account going forward, such as the trusted contact or another authorized individual.

No, you can't switch an existing account from one child to another child. The Trump Account is legally owned by the child for whom the election to open the account was made on IRS Form 4547. Only one Trump Account is permitted per child.

Trump Accounts generally remain open until the beneficiary reaches age 18. In limited circumstances, an account may be transferred or closed.

Account transfers. A Trump Account remains active and may be issued a new account number in the following circumstances:

- Change in responsible party. To help protect your child’s account, a new account number will be issued when responsibility for the account changes. This helps ensure the previous responsible party can no longer access the account.

- Transfer (rollover) to another authorized Trump Account trustee (when available).

Account closures. A Trump Account may be closed only in limited circumstances, such as:

- Death of the beneficiary.

- Rollover to an ABLE account.

- After the beneficiary reaches age 18, the assets in the account are transferred to a traditional IRA,—at which point the Trump Account is closed.

Unfunded Trump Accounts generally remain open so they can receive future contributions. If an account still has a $0 balance when the beneficiary reaches age 18, the account will be closed.

FAQ for kids

When you reach age 18, your account will transition to and follow the standard rules of a traditional IRA. You will then be able to continue to save or withdraw money from your account. If you make a withdrawal, you can use the money for certain eligible expenses, such as higher education or a down payment on a first-time home purchase (up to a $10,000 lifetime), subject to ordinary income tax but without an additional distribution tax. As with any traditional IRA, withdrawals for other, unqualified expenses would be subject to an additional 10% early distribution tax until you reach age 59½.

If you choose to save, any assets that remain in your account, will remain invested and continue to grow over time, providing potential long-term financial security.

Yes! You can view account details just like your parents can. Ask your parents to show you how.

When you reach age 18, you assume management and control of the account and will be prompted to set up your own account login information. At this point, your Trump Account will transition to a traditional IRA, since you will no longer be a minor. Also, the Responsible Party (your parent or other authorized individual) who previously managed the account on your behalf will no longer have access to it.

Yes! You may contribute your own money to your Trump Account before the account transitions to a traditional IRA when you turn 18. For example, you may choose to contribute your own savings using an eligible funding method available in the Trump Accounts app. These contributions count toward the account’s annual $5,000 contribution limit.

When you reach age 18 and your Trump Account transitions to a traditional IRA, you may continue making contributions, subject to the eligibility requirements (including earned income requirements) and annual contribution limits that apply to traditional IRAs. For details, review IRS’s IRA contribution limits.

If you want to link your bank account or debit card to contribute to your Trump Account, we’ll send you instructions by email and in the app once your account is active and able to accept contributions.

FAQ for employers and philanthropists

Employers can make contributions as part of an employee benefits program directly into eligible children’s Trump Accounts. Consult your benefits provider for additional information.

Trump Accounts and employer contributions to Trump Accounts are generally not considered “employee pension benefit plans” for purposes of ERISA. See DOL Technical Release 2026-02 for more information.

Yes. Employers can add Trump Account contributions to their Section 125 plan (Cafeteria plan) benefits so that their employees can make contributions up to the annual limit ($2,500 in 2026) for their dependents as salary reductions on a pre-tax basis.

Employers can contribute up to $2,500 per employee per year across all of an employee’s children’s Trump Accounts. If an employee has more than one child with an account, this limit applies to all their children’s accounts, not individually but as a whole. This amount counts toward the $5,000 annual limit on total private contributions for each child. Federal government contributions do not count toward this limit.

Employer contributions of up to $2,500 are excluded from the employee's gross income, providing a tax-advantaged benefit.

Philanthropists can support Trump Accounts through Treasury‑facilitated giving or independent giving, depending on their goals and structure. Visit trumpaccount.gov for more details.

Disclosures

We do not provide tax advice. For specific questions, consult a tax professional.